CMI State of the Market: Home Prices Continue to Surge at the Start of 2022

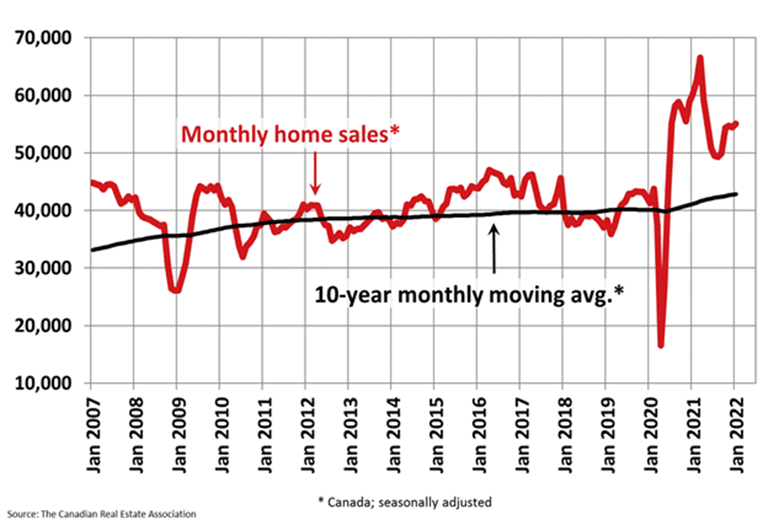

Canadian home sales edged up slightly in January, as a dearth of available supply limited real estate transactions at the start of the year. Supply constraints also helped push prices to their highest level on record, further eroding affordability at a time when mortgage rates are expected to rise.

Home Sales Edge Up in January as Prices Soar: CREA

Despite tighter supply conditions, national home sales increased 1% in January, according to the Canadian Real Estate Association (CREA). The number of newly listed properties fell 11% compared with December. Overall sales were down 10.7% from their peak in January 2021.

The MLS Home Price Index (HPI) rose at a record 2.9% pace in January, which translated into a 28% year-over-year gain – also a record. According to RBC Economics, Toronto just overtook Vancouver as Canada’s priciest housing market. Citing MLS HPI data, Toronto’s average residential property value reached $1.260 million in January compared with Vancouver’s $1.255 million.[1] A steady 5-month rise in Toronto’s composite benchmark price fuelled the surge, including a 4.3% increase in January alone.

CREA chair Cliff Stevenson said January’s limited listings were expected and that supply conditions are likely to improve in the spring season. However, the key question is “will that supply be overwhelmed by demand as it was last spring, or will we start to see the re-emergence of some of the many would-be sellers who have been hunkered down for the last two years?”[2]

Monthly home sales in Canada remain well above their long-running average. | Source: CREA

Canada’s housing market will stay strong in 2022: RBC Economics

Housing market conditions in Canada are expected to cool in the coming months but the underlying trend remains strong as unmet demand continues to fuel activity across the country, according to RBC Economics. The bank said it expects Canada’s existing housing market to generate 579,600 transactions this year, down 13.1% from the record-breaking 667,000 transactions in 2021. RBC Economics indicated that housing demand will likely prove resilient in the face of rising mortgage rates and the possibility of anti-speculation measures from Ottawa.[3]

Labor Market Sheds Jobs in January

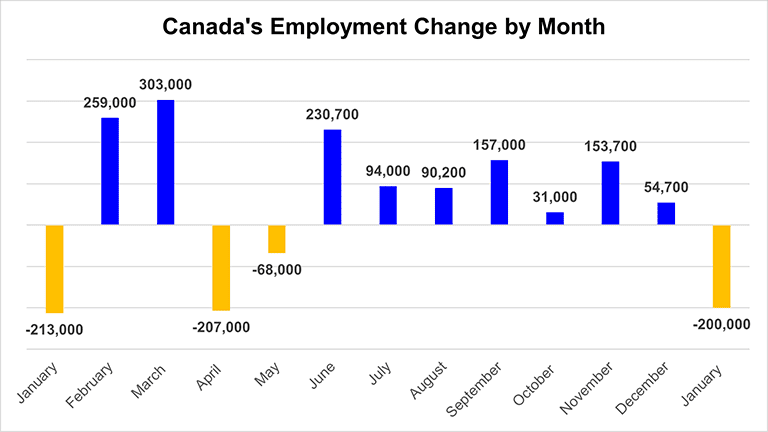

The Canadian economy lost 200,000 jobs in January as the unemployment rate rose 0.5 percentage points to 6.5%, according to official government data. The job losses were fueled by governments reinstating capacity restrictions to combat the spread of Omicron. The restrictions also impacted people who remained on payrolls during the month, as the number of workers who were employed but worked less than half of their normal hours increased by 620,000.[4]

After seven consecutive months of job gains, Canada’s labour market lost 200,000 positions in January. | Data source: Statistics Canada

Volatile Stock Market Shows Signs of Recovery

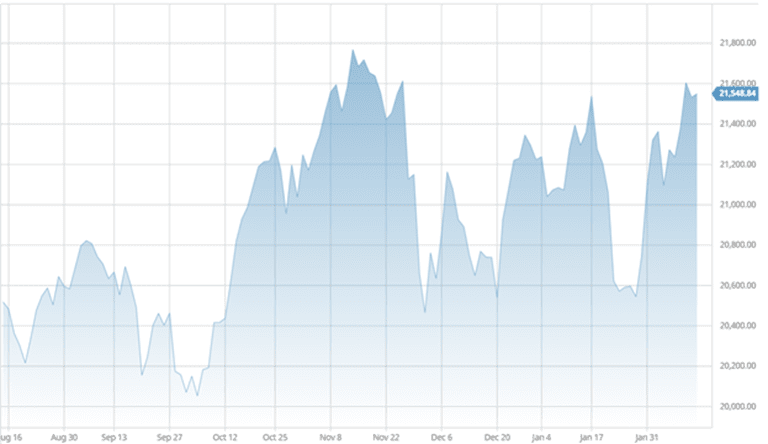

After a highly volatile start to the year, Wall Street and Canadian stocks showed signs of recovery in February as investors began pricing in better-than-expected corporate earnings. Expectations of a broad economic reopening and the end of wide-scale lockdown restrictions also fueled investors’ appetite. However, the key consideration for investors remains central-bank policy. Both the United States Federal Reserve and Bank of Canada are expected to begin raising interest rates in March to combat rising inflation. Tighter monetary policy could provide short-term headwinds to risk assets such as stocks.

Toronto’s benchmark TSX Composite Index has recovered from its yearly lows. | Source: barchart.com

Conclusion and Summary

Central-bank policy will continue to fuel market sentiment in the short term, with the prospect of higher interest rates and tighter liquidity conditions likely to influence investors’ appetite for risk assets. Income investors are similarly bracing themselves as rising rates threaten to drive down the value of bonds and interest-sensitive stocks, and erode the purchasing power of their investment income. The search for yield – already well established after a prolonged period of historically low rates – is certain to accelerate as the threat of inflation looms.

Rising interest rates have an indirect impact on mortgage rates as banks and other traditional lenders pass on the higher costs to consumers. In Canada, this scenario is unlikely to hinder market activity given strong underlying demand and a lack of available supply.

What Happens Next?

CMI Financial Group will continue to analyze market changes and keep you updated on a regular basis. Learn more about investing in private mortgages.